[ad_1]

Whereas mounted revenue traders obtained a pleasant present from the Federal Reserve within the remaining quarter of 2023, we expect a greater strategy to assess complete returns is wanting on the cumulative affect of Fed Rate hikes. On March 17, 2022, the Fed kicked off a dramatic tightening cycle from zero to five.25%–5.50% so as to carry down inflation. In latest weeks, the main focus appears to have shifted from charge hikes to rate cuts. What has this meant for markets? Partly two of this collection, we assess the dangers in mounted revenue markets and talk about a few of our greatest concepts for 2024.

Glass Half-Empty or Half-Full?

The beauty of mounted revenue investing is that returns typically exhibit a middle of gravity round yields. Firstly of the Fed charge hike cycle, yields have been close to all-time lows. What ensued was one of the crucial difficult environments for mounted revenue traders in historical past. At this time, we’re nonetheless at among the highest yields we’ve seen in fairly a while. Sadly, returns in all flavors of mounted revenue have underperformed money. Whereas we all know that bond returns are inversely correlated with rates of interest, returns for the reason that Fed began mountain climbing have resulted in meaningfully detrimental returns for core holdings just like the Bloomberg U.S. Aggregate Bond Index (Agg). High yield typically outperformed on account of tightening credit score spreads and a shorter period than investment-grade benchmarks just like the Agg.

Fastened Earnings Efficiency: 3/17/22–2/7/24

For definitions of phrases within the chart above, please go to the glossary.

Drivers of Return

Bond yields throughout the yield curve stay increased than when the Fed began mountain climbing. This implies rate of interest threat has not added worth over this era. Nevertheless, we really feel assured that the max drawdown for mounted revenue has handed. The query now’s how a lot to increase period. That is tough given the yield curve continues to be inverted, which means that any guess in longer period has a timing ingredient of when yields will fall. With hindsight, we all know that 5% was an excellent time to put money into 10-year Treasuries, however what about at the moment? In our view, sustaining a shorter period place may repay ought to the Fed not reduce charges as aggressively because the market is hoping. Within the meantime, traders derive a carry profit by investing at shorter tenors.

Affect of Credit score

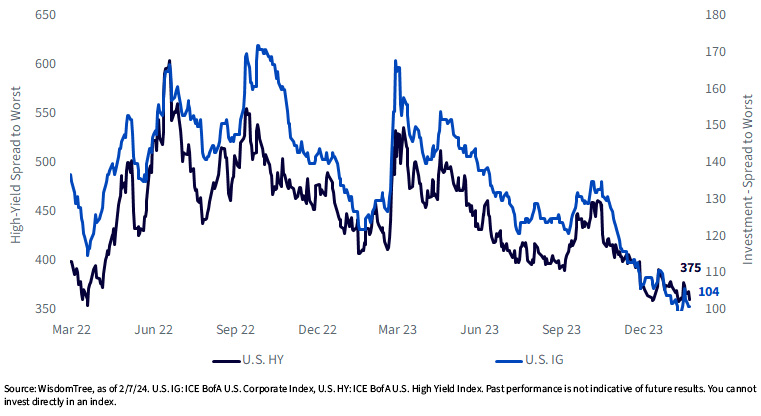

With fairness markets all over the world close to all-time highs, it needs to be no shock that credit score spreads are at among the tightest ranges of the cycle. With issues about credit score typically subdued, we nonetheless like being over-weight. Nevertheless, excessive yield might require a barely extra defensive positioning. Buyers in index-based high-yield methods are successfully betting that credit score circumstances will proceed to enhance. Whereas that is potential, it additionally exposes traders to returns which are extra correlated to threat markets like equities.

U.S. Credit score Spreads: 3/17/22–2/7/24

For definitions of phrases within the chart above, please go to the glossary.

Prime Concepts

Whereas we proceed to be sturdy proponents of the WisdomTree Floating Rate Treasury Fund (USFR), traders seeking to lengthen period in a risk-conscious method also needs to think about the WisdomTree U.S. Short-Term Corporate Bond Fund (SFIG). Whereas the lengthy finish could also be inclined to bouts of volatility from the Fed, we view the shorter finish of the curve as a relatively safer guess. Moreover, whereas credit score might not essentially be low-cost, we consider that our elementary strategy can add worth ought to fundamentals start to deteriorate. At 100 foundation factors over Treasuries, we expect investment-grade corporates on the brief finish of the curve have the potential to outperform money with solely incremental threat in 2024.

Essential Dangers Associated to this Article

There are dangers related to investing, together with the potential lack of principal.

USFR: Securities with floating charges could be much less delicate to rate of interest modifications than securities with mounted rates of interest, however might decline in worth. Fastened revenue securities will usually decline in worth as rates of interest rise. The worth of an funding within the Fund might change shortly and with out warning in response to issuer or counterparty defaults and modifications within the credit score scores of the Fund’s portfolio investments. Because of the funding technique of this Fund it might make increased capital achieve distributions than different ETFs. Please learn the Fund’s prospectus for particular particulars relating to the Fund’s threat profile.

SFIG: Fastened revenue investments are topic to rate of interest threat; their worth will usually decline as rates of interest rise. Fastened revenue investments are additionally topic to credit score threat, the chance that the issuer of a bond will fail to pay curiosity and principal in a well timed method or that detrimental perceptions of the issuer’s means to make such funds will trigger the value of that bond to say no. Whereas the Fund makes an attempt to restrict credit score and counterparty publicity, the worth of an funding within the Fund might change shortly and with out warning in response to issuer or counterparty defaults and modifications within the credit score scores of the Fund’s portfolio investments. Please learn the Fund’s prospectus for particular particulars relating to the Fund’s threat profile.

[ad_2]

Source link